Economic reports that were delayed due to the government shutdown have trickled in to reveal the economy slowed a bit more than expected in early 2019, reports Raymond James Chief Economist Scott Brown. However, the recent conclusion of the Mueller investigation with no pending indictments should serve as a market positive, according to Ed Mills, Raymond James managing director and Washington policy analyst.

In addition, it seems the Trump administration is prepared to continue negotiating with Beijing on trade, and the S&P 500 index had its best quarter since 2009, according to Bloomberg. This may be supported by a healthy labor market, as suggested by a two-month low in filings for U.S. unemployment benefits in the week ended March 23.

While most Federal Reserve policymakers expect to leave short-term interest rates unchanged over the course of the year, the federal funds futures market is pricing in about a 65% chance that the Fed will cut rates by the end of the year, explains Brown. He thinks the economy will continue to advance in 2019, but at a slower pace than last year with risks to that outlook tilted to the downside. Much has been made of a flattening yield curve, and it bears watching if the pattern sustains itself over an extended period of time.

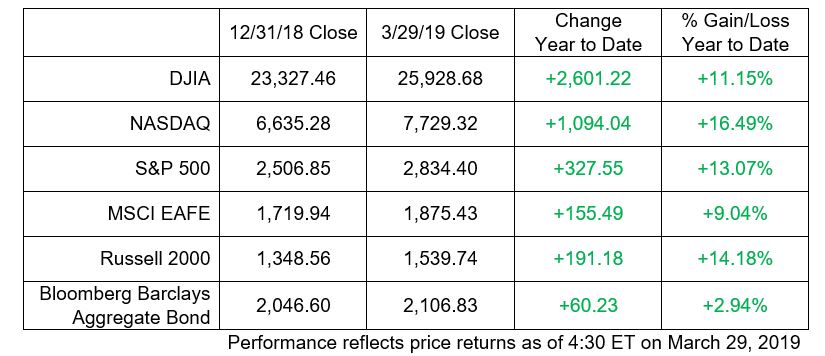

The quarter ended positively, as did the month, for the Dow Jones Industrial Average, NASDAQ and S&P 500. The Russell 2000 Index also ended positively for the quarter, but negative for the month.

Here is a look at what’s happening in the economy and capital markets, as well as key factors we are watching:

Economy

- The Mueller investigation conclusion may have a real impact on President Trump’s remaining first-term agenda, particularly on trade negotiations with China and domestic issues such as the budget or infrastructure, reports Mills.

- Slower global growth and trade policy uncertainty have weighed against business fixed investment, reports Brown. Orders and shipments of nondefense capital goods were on a softer track into early 2019; however, consumer spending growth should continue to lead the economic expansion this year.

- As mentioned above, the Fed has tabled its hopes of normalizing or raising interest rates, reports Doug Drabik, managing director, Fixed Income Research.

- The odds of a recession are about 25% in the next 12 months, shares Brown. It’s not the most likely scenario, but too high for comfort, and the odds would rise if the curve further inverts, he notes.

Equities

- The inverted yield curve deserves investor attention, states Joey Madere, senior portfolio analyst, Equity Portfolio & Technical Strategy. However, he cautions investors from overreacting, as more time is needed to see if the inversion deepens, is longer lasting and if economic disappointments start to build. Right now, the economic data reflects a slowdown, not a contraction.

- Madere states that earnings expectations also reflect some slowing, natural following the 22% earnings growth received in 2018. However, he views underlying growth as still supportive for the S&P 500 in Q1 and full year 2019.

- Valuation is fair and still has room to expand given the low inflation and interest rate environment, explains Madere. However, the inverted yield curve and slowing macro will likely keep a lid on meaningful multiple expansion.

Fixed income

- Weak European data and waning domestic growth estimates have caused investors to gravitate toward more conservative assets, Drabik adds. The change in investor flow is contributing to a back-and-forth “toying” with a three-month to 10-year Treasury inversion, although many argue that the curve reflects government intervention, as well.

- Global interest rate disparity continues with U.S. domestic rates significantly higher across the curve than many major economic powers in Europe and Asia. As inflation expectations remain muted, Drabik expects low range bond rates to continue.

International

- After a strong performance during the first two months of the year, markets outside of the United States were pressured a little during This led to certain German and Japanese government bonds to trade at a negative yield and more volatile trading in equity markets, reports European Strategist Chris Bailey. Moving certain debates forward – including Brexit – may help build investor confidence.

- A Brexit compromise still remains likely and a slight delay was negotiated, but the continuing passage of time increases the risk of less straightforward outcomes.

- According to Brown, continued geopolitical tumult along with further signs of softening in the global economy have pushed long-term interest rates lower outside of the U.S., resulting in falling domestic bond yields as global investors seek a higher rate of return.

- China reported its lowest economic growth target in a generation – still a high level compared to most other global economies. The bounce-back performance of both the Chinese financial market and local currency bodes well for 2019, so far.

Bottom line

- Madere and his team hold a positive equity market stance until more evidence of a contraction appears.

- Bailey feels global investments outside of the U.S. continue to offer potential diversification opportunities, particularly if the dollar fades in value versus other major currencies in the world.

- According to Drabik, the corporate and municipal curves have maintained positive slopes and are viable sources for fixed income allocations.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates, Inc., and are subject to change. Past performance is not an indication of future results and there is no assurance that any of the forecasts mentioned will occur. The process of rebalancing may result in tax consequences. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australia, Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. International investing involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets. Small and mid-cap securities generally involve greater risks. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. The performance noted does not include fees or charges, which would reduce an investor’s returns. Asset allocation and diversification do not guarantee a profit nor protect against a loss. Debt securities are subject to credit risk. A downgrade in an issuer’s credit rating or other adverse news about an issuer can reduce the market value of that issuer’s securities. When interest rates rise, the market value of these bonds will decline, and vice versa. U.S. Treasury securities are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return and guaranteed principal value. The yield curve is a graphic depiction of the relationship between the yield on bonds of the same credit quality but different maturities. Chris Bailey is with Raymond James Euro Equities, an affiliate of Raymond James & Associates, and Raymond James Financial Services. Material prepared by Raymond James for use by its advisors.

To opt out of receiving future emails from us, please reply to this email with the word “Unsubscribe” in the subject line. The information contained within this commercial email has been obtained from sources considered reliable, but we do not guarantee the foregoing material is accurate or complete.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC.

© 2019 Raymond James Financial Services, Inc., member FINRA/SIPC. Investment Advisory Services offered through Raymond James Financial Services Advisors, Inc.

Raymond James Financial Services does not accept orders and/or instructions regarding your account by email, voice mail, fax or any alternate method. Transactional details do not supersede normal trade confirmations or statements. Email sent through the Internet is not secure or confidential. Raymond James Financial Services reserves the right to monitor all email. Any information provided in this email has been prepared from sources believed to be reliable, but is not guaranteed by Raymond James Financial Services and is not a complete summary or statement of all available data necessary for making an investment decision. Any information provided is for informational purposes only and does not constitute a recommendation. Raymond James Financial Services and its employees may own options, rights or warrants to purchase any of the securities mentioned in this email. This email is intended only for the person or entity to which it is addressed and may contain confidential and/or privileged material. Any review, retransmission, dissemination or other use of, or taking of any action in reliance upon, this information by persons or entities other than the intended recipient is prohibited. If you received this message in error, please contact the sender immediately and delete the material from your computer.