Trade tensions reached a new pitch Friday when the Trump administration announced a 25% tariff on all exports from Mexico by October, shares Washington Policy Analyst Ed Mills. Further, China released a white paper over the weekend that Mills and his team view as a signal toward a prolonged U.S.-China trade war. This follows President Trump raising the 10% tariff on $200 billion in Chinese goods to 25% and his threats to impose further tariffs on an additional $300 billion or so in Chinese goods, explains Raymond James Chief Economist Scott Brown. It doesn’t appear that trade tensions will abate soon, he adds, as the U.S. has begun to restrict access for specific companies, such as Huawei, while China has threatened to cut off access to its market for rare earth minerals. These are critical to the production of technology goods, and China controls 80% of the world’s supply.

Eyes will be on the G-20 meeting at the end of June to further U.S.-China trade negotiations. However, Mills and his team believe it’s possible that a coinciding meeting between Presidents Trump and Xi will not take place, which could increase the chances that the additional proposed tariffs would go into effect. Some Federal Reserve (Fed) officials have concerns about the effects of tariffs on inflation; however, that should be temporary, says Brown. He thinks the drag on overall economic growth will be more significant.

Brown says the Fed has sent a clear signal that it will be patient in deciding its next policy move. The federal funds futures market is pricing in a strong chance of one or more interest rate cuts by the end of the year, he adds. Mills points to significant movement on key domestic issues such as increasing federal budget spending and ratifying the United States-Mexico-Canada Agreement as potential market positives. He thinks checking these items off their to-do list would be a win for the Trump administration that could strengthen the U.S. position in trade negotiations.

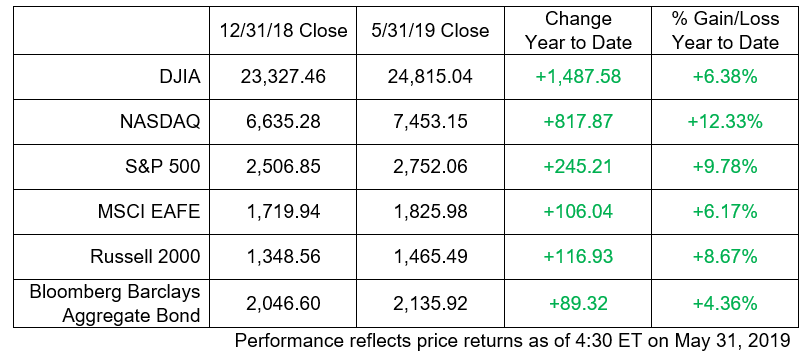

Following recent volatility, the month ended negatively for the Dow Jones Industrial Average, NASDAQ, S&P 500 and the Russell 2000 Index.

Here is a look at what’s happening in the markets both here and abroad, as well as key factors we are watching:

Economy

- Anecdotal evidence indicates that tariffs have slowed overall economic growth, Brown shares. Researchers at the Federal Reserve Bank of New York estimate that the annual cost of tariffs imposed to date amount to over 2% of average household income.

- While headline gross domestic product growth was relatively strong in the first quarter, that figure was boosted by net exports and an increase in inventory accumulation, Brown explains. Consumer spending and business fixed investment grew at a lackluster pace and residential fixed investment fell for the fifth consecutive quarter. April data on retail sales and industrial production failed to signal much of a pickup into the second quarter.

- The U.S. economy has held up better than many other places in the world over the past 12 months, says Joey Madere, senior portfolio strategist, Equity Portfolio & Technical Strategy. However, trade disputes pushed the May U.S. manufacturing Purchasing Managers Index (PMI) to its lowest level in nearly 10 years.

Equities

- First-quarter earnings were much better than expected, says Madere, driven by companies with more exposure to the U.S. For example, S&P 500 companies with over 50% of revenues from the U.S. exhibited 5.6% sales growth and 8.1% earnings growth on average in the first quarter, whereas those with over 50% of revenues from overseas grew sales and earnings by an average of 2.1% and 4.0% respectively, he explains.

- Looking forward, Madere says earnings growth expectations are similar for these two groups over the next 12 months. Of course, higher tariffs have the ability to impact global growth and corporate margins if they go into effect.

- Madere believes it is important to manage global exposure within your portfolios, especially in the current environment. Trade negotiations will remain the key influence to monitor.

- With continued trade tensions and difficulty for progress in the near term, Madere and his team feel that equities are likely to be range bound until trade negotiations can show signs of positive momentum. In the short term, we look for downside technical support in the 2,680-2,740 area.

Fixed income

- Senior fixed income strategist Doug Drabik cautions that an extended yield curve inversion may be a warning sign of a possible recession. During the last three inverted curves, bonds rallied across the curve. During the last three recessions, however, bonds also rallied but more significantly on the short end (meaning short-term yields dropped precipitously). This appears to be part of the normal economic cycle that eventually leads to a positively sloped yield curve.

- Over the same time period, stocks dropped in value, emphasizing the importance of keeping a balanced asset allocation, Drabik adds.

- According to Nick Lacy, chief portfolio strategist for Raymond James Asset Management Services, all U.S. Treasury yields are below cash interest rates except the 30-year bonds. While the two-year rate is still higher than the 10-year rate, it is still a problem in his view.

International

- May was a weak month for international markets as global trade tensions impacted investor confidence in risk assets, including equities and commodities, European Strategist Chris Bailey explains.

- In Europe, parliamentary elections displayed a more fragmented voting population with support shifting from centrist politics to both populist parties and other alternatives, including ecologically friendly Green parties and pro-European liberal parties, Bailey says.

- Theresa May’s resignation has spurred a race for her successor, which Bailey says is not likely to conclude until July.

- Pan-European assets remain low-valued in comparison to other developed market peers. Bailey is waiting for more political clarity and global trade progress before making further predictions.

- Lacy and his team still prefer developed foreign markets over emerging markets. If emerging markets continue to decline, they would become far more attractive opportunities, but that’s not the case yet, he explains.

Bottom line

- Madere expects volatility to increase in the coming weeks and believes investors should remain patient to take advantage of buying opportunities during weaker periods.

- Lacy believes the current market environment offers investors the chance to increase their exposure to high-quality stocks and bonds. Within stocks, he recommends owning more large-cap stocks and lower volatility stocks, such as dividend-paying stocks or defensive sectors.

- We continue to believe that a diversified asset allocation is crucial to helping investors ensure their portfolios stay balanced over time and in various market conditions.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates, Inc., and are subject to change. Past performance is not an indication of future results and there is no assurance that any of the forecasts mentioned will occur. The process of rebalancing may result in tax consequences. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australia, Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. The Purchasing Managers Index (PMI) is a measure of the prevailing direction of economic trends in manufacturing. An investment cannot be made in these indexes. International investing involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets. Small and mid-cap securities generally involve greater risks. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. The performance noted does not include fees or charges, which would reduce an investor’s returns. Asset allocation and diversification do not guarantee a profit nor protect against a loss. Debt securities are subject to credit risk. A downgrade in an issuer’s credit rating or other adverse news about an issuer can reduce the market value of that issuer’s securities. When interest rates rise, the market value of these bonds will decline, and vice versa. U.S. Treasury securities are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return and guaranteed principal value. The yield curve is a graphic depiction of the relationship between the yield on bonds of the same credit quality but different maturities. Chris Bailey is with Raymond James Investment Services. Material prepared by Raymond James for use by its advisors.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC.

© 2019 Raymond James Financial Services, Inc., member FINRA/SIPC. Investment advisory services offered through Raymond James Financial Services Advisors, Inc.