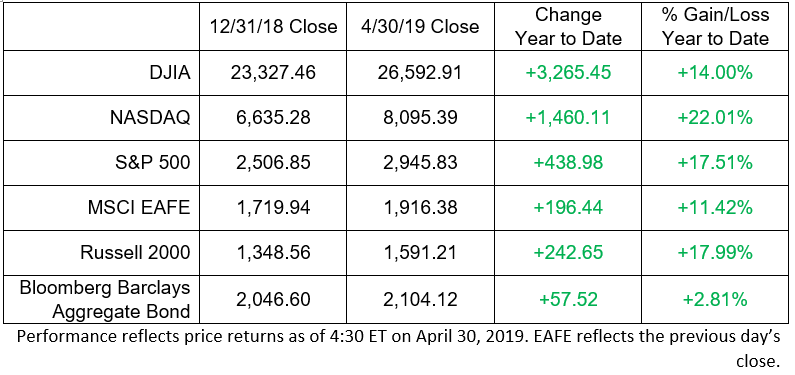

On the back of solid first-quarter earnings results and healthy economic data releases, the S&P 500 continued its remarkable move higher and closed at a record high for the first time since September 2018, shares Chief Investment Officer Larry Adam. To put the strength of the rally into perspective, the S&P 500 is now up 17.5% year-to-date through April 30, which marks the best start to a year since 1975 and the second best over the last 75 years, he said.

While Gross Domestic Product (GDP) rose at a 3.2% annual rate in the advance estimate for the first quarter of 2019, the details of the report were a mixed bag, explains Chief Economist Scott Brown. Growth was stronger than expected; however, it was boosted by faster inventory growth and a narrower trade deficit – both of which he believes are likely to reverse in the second quarter.

The Federal Reserve (Fed) is expected to keep short-term interest rates steady for the foreseeable future. Fed officials are reviewing monetary policy strategies, tools and communications policies this year, but changes aren’t expected until 2020, Brown added. All of this, combined with positive first-quarter earnings (78% of companies saw an average earnings surprise of 6.33%, adds Senior Portfolio Strategist Joey Madere) and a steepening yield curve, has made this year a good one for diversified portfolios up to this point, says Chief Portfolio Strategist Nick Lacy.

The month ended positively for the Dow Jones Industrial Average, NASDAQ, S&P 500 and the Russell 2000 Index.

Here is a look at what’s happening in the economy and capital markets, as well as key factors we are watching:

Economy

- First-quarter softness in underlying domestic demand may have reflected an impact from the partial government shutdown, explains Brown. Key components of the economy are expected to rebound in the second quarter.

- Growth is expected to be moderate in 2019; however, the risks are weighted to the downside.

- Consumer spending and business fixed investment slowed, while residential fixed investment fell for the fifth consecutive quarter, he adds.

- Inflation has remained below the 2% target. The Fed could cut interest rates in the months ahead if the labor market begins to weaken; however, no changes are expected until 2020.

Equities

- After rising approximately 10% year-over-year in 2018, dividends are expected to grow an additional 7% in 2019 to another record high, explains Adam. As the current S&P 500 dividend yield (+1.9%) remains elevated relative to short-term Treasury yields, U.S. equities remain an attractive investment in his view.

- First-quarter earnings have been well-received, with notable strength from the technology-oriented areas, explains Madere.

- Seven of the 11 S&P sectors have risen above their September highs. The largest percentage of Q1 earnings beats have come from the Technology, Consumer Discretionary, Communication Services, and Consumer Staples sectors so far. Communication Services has stood out in terms of average price reaction to earnings results.

- Another sign of economic strength, in Madere’s view, is that 73% of S&P 500 stocks are above their 200-day moving average. Readings above 80% have often coincided with short-term pauses or peaks, so there is still room for upside in the short term. Additionally, we believe potential pullbacks should be normal in nature.

Fixed income

- The world’s central banks have all remained constant in their current monetary policies. And it appears the Fed isn’t expected to make policy changes either, according to Doug Drabik, senior fixed income strategist.

- The bond market sold off at the beginning of the month, pushing yields 5 basis points higher in the intermediate part of the curve and approximately 12 basis points out on the longer end of the curve.

- The municipal and corporate curves maintained a positive slope. The small narrowing in product spreads for the month was offset by the Treasury curve sell-off (yield increases).

- The “sweet” spot of the municipal curve has drifted to the 11- to 18-year maturity range, where 75% to 90% of the entire curve’s yield can be captured, according to Drabik. The same opportunity for yield can be found among corporate bonds in the 5- to 12-year maturity range.

- While some investors are lamenting low rates, according to managing director Ted Ruddock, they may be missing opportunities in the municipal market that is rewarding investors for extending maturities but managing duration risk with embedded call options.

International

- Global equity markets continued to make progress in April, shares European Strategist Chris Bailey, distancing themselves from December 2018 lows despite a rising dollar and a lack of overt progress in key geopolitical debates, including the U.S./China trade discussions and Brexit.

- April saw some downbeat comments from the European Central Bank about the eurozone’s economic progress and continuing difficult manufacturing output and sentiment data in Asia, he adds.

- April also saw heightened volatility in Turkey and Argentina, while both Brazil and China made positive progress on legislation to help boost economic dynamism, Bailey explains. Toward the end of the month, the global corporate earnings season started solidly in both Europe and Asia.

Bottom line

- Adam and the Investment Strategy team remain constructive on the equity market long-term and would use any near-term weakness as a buying opportunity.

- Drabik feels that Treasuries remain a viable option for short-term planning, especially in high-income states, since they are federally taxable but exempt from state income taxes.

- According to Madere, the S&P 500 holding its new high (without a quick rollover) is a good marker for continued momentum, which is what he and his team will be monitoring next.

Investing involves risk, and investors may incur a profit or a loss. All expressions of opinion reflect the judgment of the Research Department of Raymond James & Associates, Inc., and are subject to change. Past performance is not an indication of future results and there is no assurance that any of the forecasts mentioned will occur. The process of rebalancing may result in tax consequences. Economic and market conditions are subject to change. The Dow Jones Industrial Average is an unmanaged index of 30 widely held stocks. The NASDAQ Composite Index is an unmanaged index of all common stocks listed on the NASDAQ National Stock Market. The S&P 500 is an unmanaged index of 500 widely held stocks. The MSCI EAFE (Europe, Australia, Far East) index is an unmanaged index that is generally considered representative of the international stock market. The Russell 2000 is an unmanaged index of small cap securities. The Bloomberg Barclays US Aggregate Bond Index is a broad-based flagship benchmark that measures the investment grade, U.S. dollar-denominated, fixed-rate taxable bond market. An investment cannot be made in these indexes. International investing involves additional risks such as currency fluctuations, differing financial accounting standards, and possible political and economic instability. These risks are greater in emerging markets. Small and mid-cap securities generally involve greater risks. Companies engaged in business related to a specific sector are subject to fierce competition and their products and services may be subject to rapid obsolescence. There are additional risks associated with investing in an individual sector, including limited diversification. The performance noted does not include fees or charges, which would reduce an investor’s returns. Asset allocation and diversification do not guarantee a profit nor protect against a loss. Debt securities are subject to credit risk. A downgrade in an issuer’s credit rating or other adverse news about an issuer can reduce the market value of that issuer’s securities. When interest rates rise, the market value of these bonds will decline, and vice versa. U.S. Treasury securities are guaranteed by the U.S. government and, if held to maturity, offer a fixed rate of return and guaranteed principal value. The yield curve is a graphic depiction of the relationship between the yield on bonds of the same credit quality but different maturities. Chris Bailey is with Raymond James Investment Services. Material prepared by Raymond James for use by its advisors.

Securities offered through Raymond James Financial Services, Inc., member FINRA/SIPC.

© 2019 Raymond James Financial Services, Inc., member FINRA/SIPC. Investment Advisory Services offered through Raymond James Financial Services Advisors, Inc.